Trading crypto wisely on Prediction market

Executive Summary

The crypto derivatives landscape has undergone a profound structural shift. While centralized exchanges (CEXs) like Binance, OKX and Deribit continue to dominate institutional volume with perpetual swap, dated futures and vanilla options, decentralized and regulated prediction markets like Polymarket and Kalshi have emerged as powerful parallel trading venue. No longer confined to political forecasting or pop-culture trivia, these platforms now offer a substitute suite of crypto-native financial products.

It can be a similar trade idea that whether Bitcoin will hit a certain price, when betting on Polymarket compared to trading call/put options on Deribit, but their payoff structures, margin requirements, liquidity profiles, and risk-reward dynamics can be quite different.

This article provides an angle to practical differences between crypto prediction market instruments and CEX options, supplemented by case study based on real market data.

With Polymarket now integrated into 1Token, institutional managers can also monitor and reconcile prediction market positions alongside their broader CeFi, DeFi and TradFi portfolios.

Core Definitions and Structural Taxonomy

To effectively navigate these markets, we must first look at the basic math behind how they pay out.

Prediction Market Contracts

At their core, contracts traded on Polymarket and Kalshi are cash-or-nothing binary options. For any given contract, a trader purchases a "Yes" or "No" share. The purchase price of a single share is bounded strictly between $0.00 and $1.00, reflecting the market's implied probability of the event occurring (e.g., a contract trading at $0.24 implies a 24% probability of occurrence).

The payoff profile is simple and fixed (or in other words, discontinuous and bounded). If the underlying event resolves as true: The "Yes" contract pays out exactly $1.00, yielding a profit of $1.00 minus Purchase Price. The "No" contract expires worthless ($0.00), resulting in a total loss of the initial premium paid.

Binary vs. Vanilla Option Payoff Profiles

Traditional options traded on platforms like Deribit are vanilla European options. Unlike binary options, their payoff at expiration is continuous and linear relative to the distance between the final spot price (S) and the strike price (K).

- Vanilla Call Option Payoff: max(0,S - K)

- Vanilla Put Option Payoff: max(0,K - S)

Vanilla Option Payoff (Deribit) Binary Option Payoff (Polymarket/Kalshi)

^ ^

| / | |--------- (Max Payout = $1)

| / | |

| / | |

----------+---/--------> Price ----------+------|--------> Price

| / (Strike K) | (Strike K)

| / |In a vanilla option, your upside is theoretically unlimited (for a call) or bounded only by the asset hitting zero (for a put). In a binary prediction market contract, your upside is rigidly capped at $1.00 per share, regardless of how far the asset price moves past the strike threshold.

Classification of Crypto Prediction Marketss

Prediction markets categorize their crypto products into distinct archetypes based on their temporal and path-dependent characteristics.

European-Style Expiry-Based Binaries

These contracts depend entirely on the asset's price at a specific, predetermined moment in time, ignoring all price action prior to expiration.

- Single-Threshold: Kalshi's "Bitcoin price today at 11pm EDT: $76,500 or above".

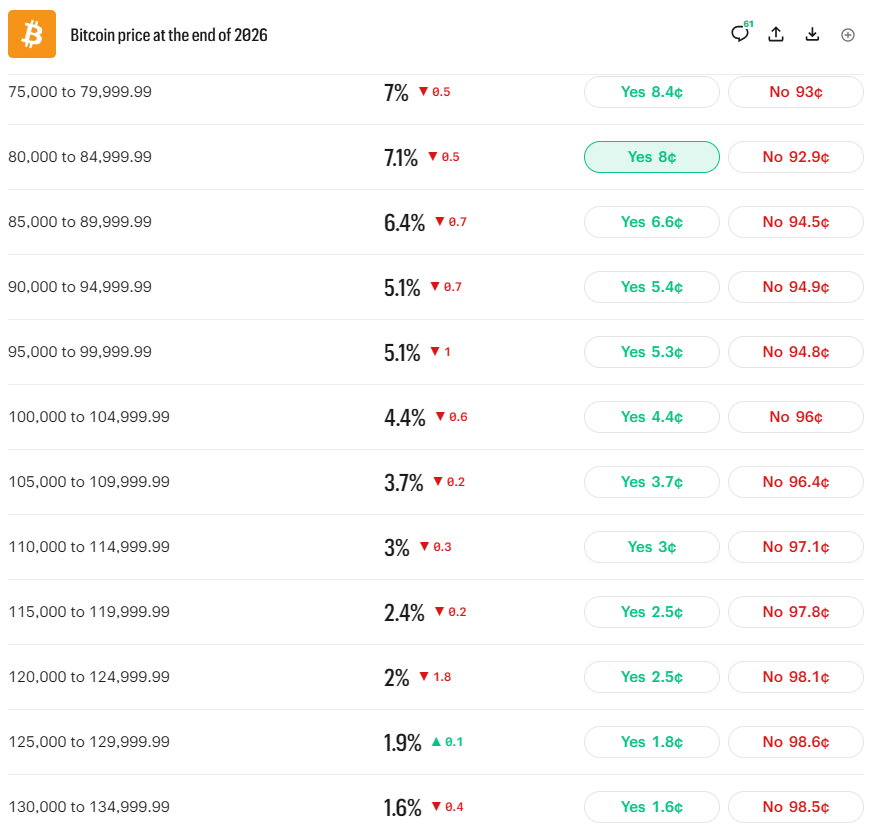

- Interval Ranges (Probability Densities): Kalshi’s "Bitcoin price at the end of 2026" broken into $5,000 increments (e.g., 75,000 to 79,999.99).

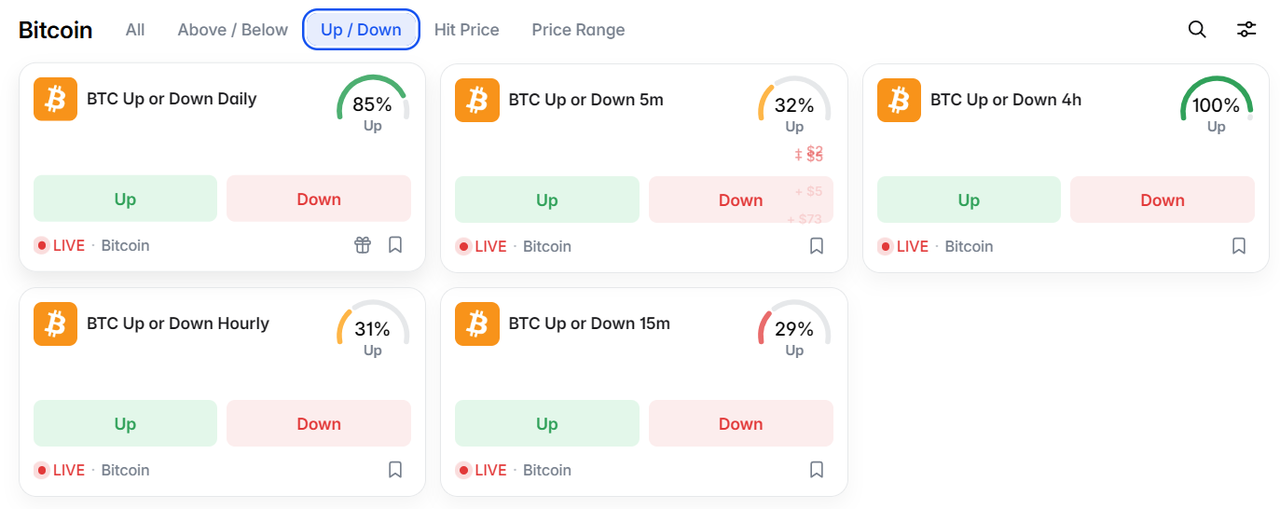

- Ultra-Short-Term: Polymarket regularly lists micro-interval contracts, such as "BTC Up or Down 5m" or "BTC Up or Down Hourly". From a financial structural standpoint, these are ultra-short-term European binary options. Dominated by order-flow noise and microstructure frictions rather than macroeconomic fundamentals, those are seen as speculative casino-style vehicles rather than systematic hedging tools.

By looking at the prices of these contiguous brackets across an entire range, traders can view a live, market-priced Probability Density Function (PDF) of Bitcoin's future price without needing to back-calculate it from vanilla option delta skews.

American-Style "Hit Price" / Barrier Binaries

Unlike expiry-based contracts, American-style prediction contracts are path-dependent. They resolve as true the exact second the underlying asset touches or crosses a specified price barrier at any point during the contract's lifespan.

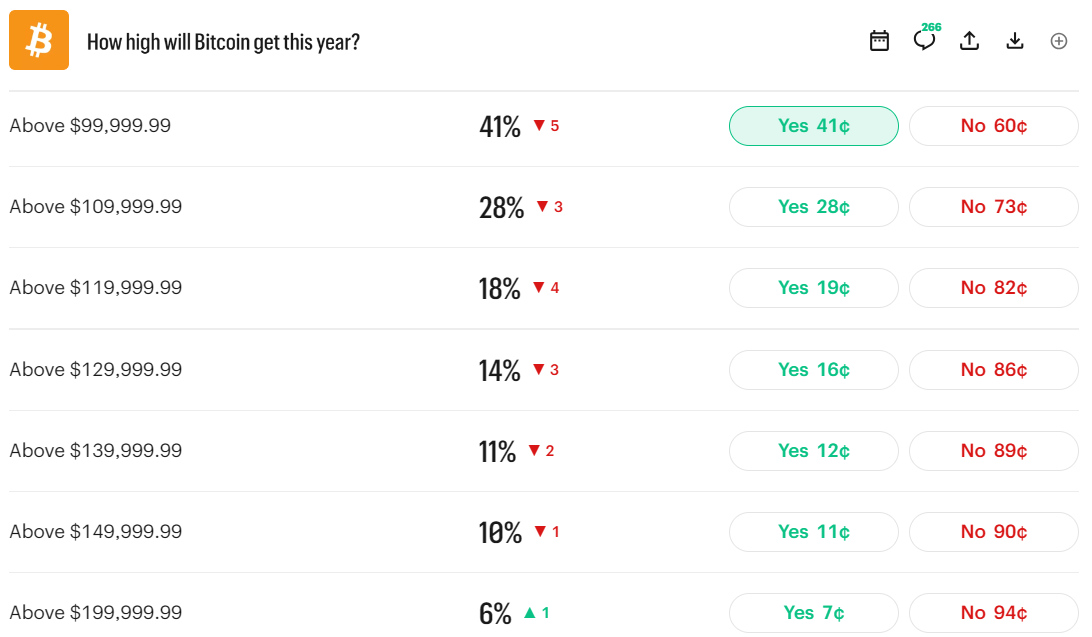

- Examples: Polymarket's "What price will Hyperliquid hit in May?" or Kalshi's "How high will Bitcoin get this year? Above $109,999.99".

In TradFi, these are known as American One-Touch Digital Calls/Puts, where pricing American barrier options requires complex adjustments for corporate actions, such as cash dividends, stock splits, and spin-offs, which cause artificial drops in the underlying stock price.

In the crypto market, however, it's easier because asset prices are driven almost exclusively by pure price volatility. Cororate actions (such as hard forks or network air-drops) are rare already (like BOBA airdrop for OMG, on average 1-2 times a year, probably less), and those cases where those actions alter the underlying spot price are also rare. This gives American binary options in crypto a clean, structurally pure pricing environment.

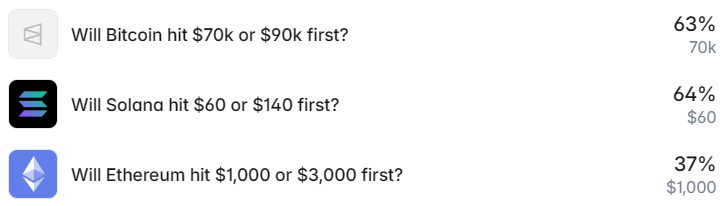

Will price hit A or B first?

For retail it's a gambling tool, but for professional institutional desks, these contracts are highly valuable for hedging conditional risks that standard linear instruments (like spot or futures) cannot solve. Here are the two most common professional use cases:

In TradFi, major OTC traders engineer these highly path-dependent products for corporate clients or hedge funds who need to manage very specific risks. E.g., You have a heavy leveraged long position buy the "70k First" YES shares on the prediction market to protect yourself on flash crash.

Exogenous Event

One of the most powerful innovations of prediction markets is the ability to trade contracts that represent systemic crypto risks that cannot be directly captured by standard centralized derivatives.

- "Will Satoshi move any Bitcoin in 2026?" (Direct proxy for supply shocks).

- "Opensea FDV above one day after launch?" (Pre-market valuation discovery tool).

- "Clarity Act signed into law in 2026?" (Regulatory and compliance risk hedging).

While a trader cannot directly hedge "regulatory hostility" on any derivatives exchange, buying "Yes" shares on a crypto regulatory framework contract allows structural market participants to build multi-asset proxy hedges for their spot altcoin portfolios.

Quantitative Case Study: Scenario & PnL Comparison

To evaluate the efficiency of these instruments, let's analyze a real-world market pricing scenario provided in research, focusing on European-style and American-style options in prediction market and CEX.

Market Conditions & Parameters

- Trade Date: May 20 2026

- Expiry Date: Year-end 2026 (Deribit settlement date at Dec 26, 2026, prediction market settlement date at Dec 31, 2026)

- BTC Spot Price: $76,780

- Total Investment Capital: 1,000 USDT (Deribit actual collateral in BTC but let's assume it's kept at 1,000 USDT, and assuming use conservative leverage on Deribit)

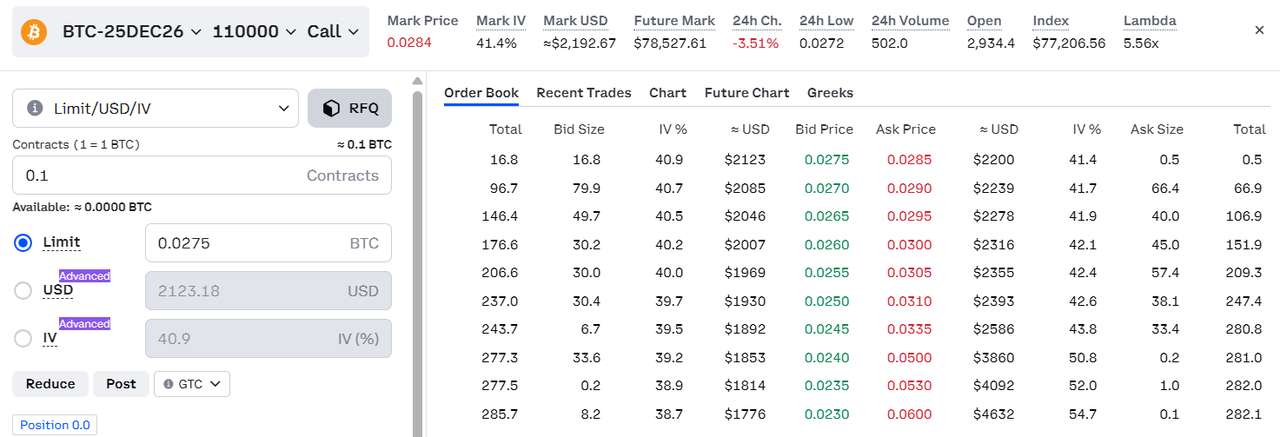

Case Study A: The $110,000 Call Threshold Analysis (Upside Skew)

We evaluate three distinct instruments targeting a bullish break past $110,000.

- American Binary Option on Prediction Market: Priced at $0.24. Resolves to $1.00 if BTC touches $110,000 at any time before year-end 2026.

- European Binary Option (no direct prediction market, but can be synthesized via a combination of bracketed range contracts): Overall priced between $0.181 and $0.194 due to the accumulative bid-ask spread. Resolves to $1.00 only if BTC settles above $110,000 at final expiration.

- Deribit European Vanilla Call (Inverse Option): Premium is 0.028 BTC

Understanding the Deribit Inverse Payoff Friction

Deribit options are BTC-margined and BTC-settled. This means the premium, collateral, and final payouts are all denominated in Bitcoin, creating a non-linear dollar PnL curvature.

When you buy a call option on a BTC-denominated platform, you are exposed to a "double long" dynamic: as the price of Bitcoin rises, the option payout in BTC increases, and the USD value of each of those BTC also increases. Conversely, the inverse structure scales down the option's payout in absolute BTC terms at extremely high prices because the option payout formula divides the USD profit by the final settlement price:

Payout (BTC)=Smax(0,S - K)

Your research explicitly states that the 1,000 USD fiat capital has been perfectly hedged against spot BTC downside exposure for the premium purchase. Let us analyze the exact mathematical outcome if Bitcoin rallies strongly and ends up at $120,000.

PnL Breakdown at Spot $120,000

- American Binary Option:

- Contracts Purchased: 0.241000 USDT = 4,166.67 shares

- Gross Payoff: 4,166.67×$1.00 = $4,166.67

- Net PnL: $3,166.67

Note: Because BTC hit $120,000, it must have crossed the $110,000 barrier, triggering a full payout.

- European Binary Option (Synthesized Combination):

- Optimistic Entry ($0.194): 0.1941000=5,154.64 shares → Net PnL = $4,154.64

- Conservative Entry ($0.181): 0.1811000=5,524.86 shares → Net PnL = $4,524.86

- Net PnL Range: $4,154.64 ~ $4,524.86

- Deribit European Vanilla Call:

- Initial margin in BTC: 0.013024 BTC

- Option Position Size (Contracts): 0.5 BTC Contracts

- Options premium paid: 0.5 * 0.028 = 0.014 BTC

- Position Payout at $120,000: 0.5 * 0.083333 = 0.04167 BTC

- Net BTC Account Change: 0.04167 BTC - 0.014 BTC = 0.02767 BTC

- USD Realized PnL (Liquidated at $120,000): 0.02767 BTC * $120,000 = $3,320.4 USD

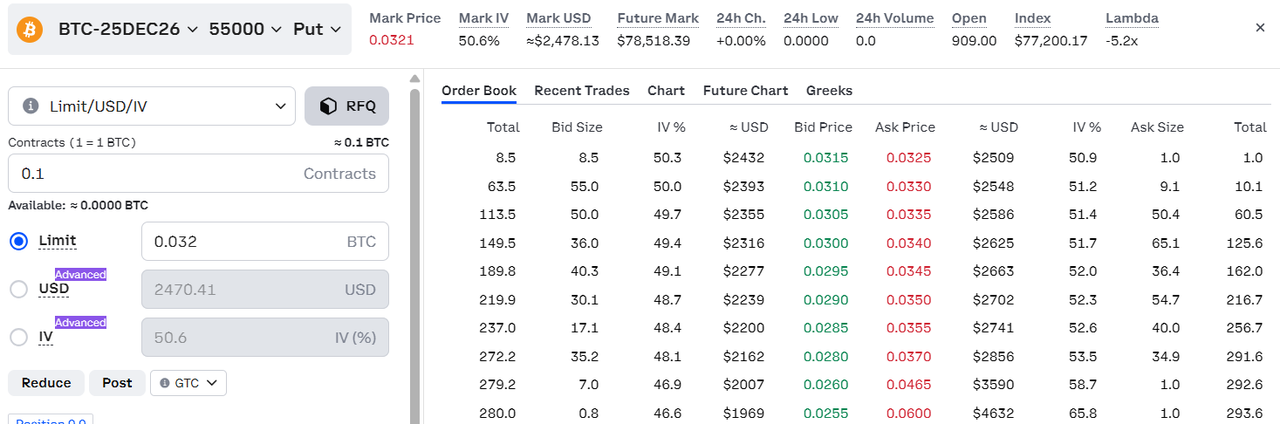

Case Study B: The $55,000 Put Threshold Analysis (Downside Protection)

We evaluate three distinct instruments targeting a bearish break below $55,000.

- American Binary Option (Hit Price): Priced at $0.50.

- European Binary Option (Synthesized): Priced between $0.155 and $0.174.

- Deribit European Vanilla Put (Inverse Option): Premium is 0.032 BTC.

We analyze the financial outcome if a severe market correction occurs and Bitcoin falls to $50,000 at expiration.PnL Breakdown at Spot $50,000

- American Binary Option:

- Contracts Purchased: 0.501000 = 2,000 shares

- Gross Payoff: 2,000×$1.00 = $2,000

- Net PnL: $1,000.00

- European Binary Option (Synthesized Combination):

- At Worst-Case Entry ($0.174): 0.1741000=5,747.13 shares → Net PnL= $4,747.13

- At Best-Case Entry ($0.155): 0.1551000=6,451.61 shares → Net PnL= $5,451.61

- Net PnL Range: $4,747.13 ~ $5,451.61

- Deribit European Vanilla Put:

- Initial margin in BTC: 0.013024 BTC

- Option Position Size (Contracts): 0.5 BTC Contracts

- Options premium paid: 0.5 * 0.032 = 0.016 BTC

- Position Payout at $50,000: 0.5 * 0.01 = 0.05 BTC

- Net BTC Account Change: 0.05 BTC - 0.016 BTC = 0.034 BTC

- USD Realized PnL (Liquidated at $120,000): 0.034 BTC * $50,000 = $1,700 USD

Strategic Insights

- Synthesized European Binary Options seems to offer the best ROI due to its lowest entry premium. It maximizes your contract count and delivers the highest terminal payout, but the payout would not be competitive if the price goes far beyond the target hit price. While if there's mispricing in relative short-term symbols, there can be an arbitrage between them.

- Buy American Binary Options if the price Hits the Target but Pulls Back before year-end. You lock in a 100% full payout the exact second BTC touches your threshold, completely protecting you if the market subsequently reverses.

Liquidity Frictions and Trading Realities

While the theoretical returns on prediction markets look exceptionally lucrative on paper, executing these strategies requires a deep understanding of structural market frictions.

Centralized Exchanges (CEX) vs. Prediction Markets Order Book Depth

Centralized venues like Deribit and Binance operate with deeply capitalized, institutional electronic market makers, automated market-making algorithms, and high-frequency trading (HFT) infrastructure. Order books feature deep liquidity, tight bid-ask spreads, and multi-million dollar block trading capacity via institutional RFQ (Request for Quote) networks.

In contrast, prediction markets exhibit significantly thinner structural depth. Liquidity is highly concentrated around major headline contracts (like political elections), while specific crypto-native price brackets suffer from low capital thickness.

Deribit Order Book (Deep, Institutional) Polymarket/Kalshi Order Book (Thin, Bounded)

Price | Size (BTC) Price | Size (Shares)

$2,185 | 23.7 27¢ | 311

$2,224 | 60.0 26¢ | 3,012

$2,262 | 62.2 25¢ | 3,035 Execution Strategies for Thinner Markets

The available depth on these prediction contract order books cannot cleanly absorb a standard mid-sized retail or institutional allocation (e.g., $10,000 USDT or greater) in a single market order without incurring devastating execution slippage.

To deploy capital efficiently on platforms like Polymarket or Kalshi without front-running yourself or moving the implied probability curve unfavorably, you must employ systematic execution algorithms:

- Time-Weighted Average Price (TWAP): Slice your target size into micro-orders (e.g., 200 USDT per chunk) executed at automated intervals over hours or days to allow organic retail liquidity to replenish the book.

- Passive Limit Order Posting: Avoid crossing the bid-ask spread. Act as a liquidity provider by placing passive limit bids inside the order book, capturing shares only when impatient market participants sell into your liquidity.

- Cross-Market Statistical Arbitrage: Keep a close eye on price misalignments between Polymarket (decentralized, crypto-native user base) and Kalshi (regulated, domestic US fiat user base). Because these two user cohorts have entirely different access capital and regional biases, identical underlying contracts frequently exhibit wide pricing gaps that can be locked in via multi-platform execution.

Strategic Asset Allocation Framework

To maximize your capital efficiency across these various venues, use the following operational matrix to match your specific market outlook with the correct financial instrument.

Summary Allocation Matrix

Definitive Trading Recommendations

Choose Centralized Vanilla Options when trading size and scale . If you are deploying serious institutional capital or looking to capture a massive macroeconomic breakout where you want your profits to scale linearly to the sky, stick to centralized options. The deep order books and institutional clearing infrastructure make them the only viable choice for major structural positioning.

Choose American Binary Options when trading aggressive path-dependent volatility. If your quantitative models indicate an impending liquidity squeeze or flash-crash that will briefly spike prices through a specific level before rapidly reverting, use the "Hit Price" contracts on Polymarket or Kalshi. This lets you bank full payouts without needing to time your exit perfectly at expiration.

Choose Synthesized European Binary Ranges for small-capacity high profitability arbitrage. As the price difference with CEX is big, while the trading target is the same, there can be an delta-neutral arbitrage chance between prediction market and CEX, however due to multiple books' spreads and insufficient depth, the execution efficiency is crucial even for small capital.

Comments ()