Crypto Quant Strategy Index IX Jan 2026

Executive Summary

This report presents an index benchmark analysis developed by 1Token in collaboration with 13 crypto trading teams. Among these partners, nine teams contributed Funding Arbitrage strategies, four teams (with some overlap) provided Long Short strategies, and four teams (with some overlap) provided directional strategies.

The comprehensive study evaluates three distinct strategy indices for January 2026, delivering key insights into Funding Arbitrage, Long Short and Directional strategy performance metrics, such as period returns, maximum drawdown, unit leverage returns, and asset concentration, aiming to provide a reference for the market.

Parameters

- Quote source: CMC

- Granularity: Daily

- Index start time: January 1st, 2026 at 00:00 UTC

- Cut-off-time: 0:00 UTC+0

- Sample Exchange Distribution: : Binance, OKX, Bybit, Gate.io, Bitget, LTP Rapidx

- Accum. NAV calculation method: TWR (Time-Weighted Return)

- Risk-free rate: 4.3% (based on avg data of US 10-Y Treasury Yield in 2025)

- Daily Minimum Acceptable Return (MAR): 0

Note: The selection of the exchanges may influence overall performance, as these platforms have different mechanisms such as fees, commissions, and slippage. Monthly index report does not take the mechanism difference into consideration, assuming no confounding variables affect the comparison.

Index

Calculation method

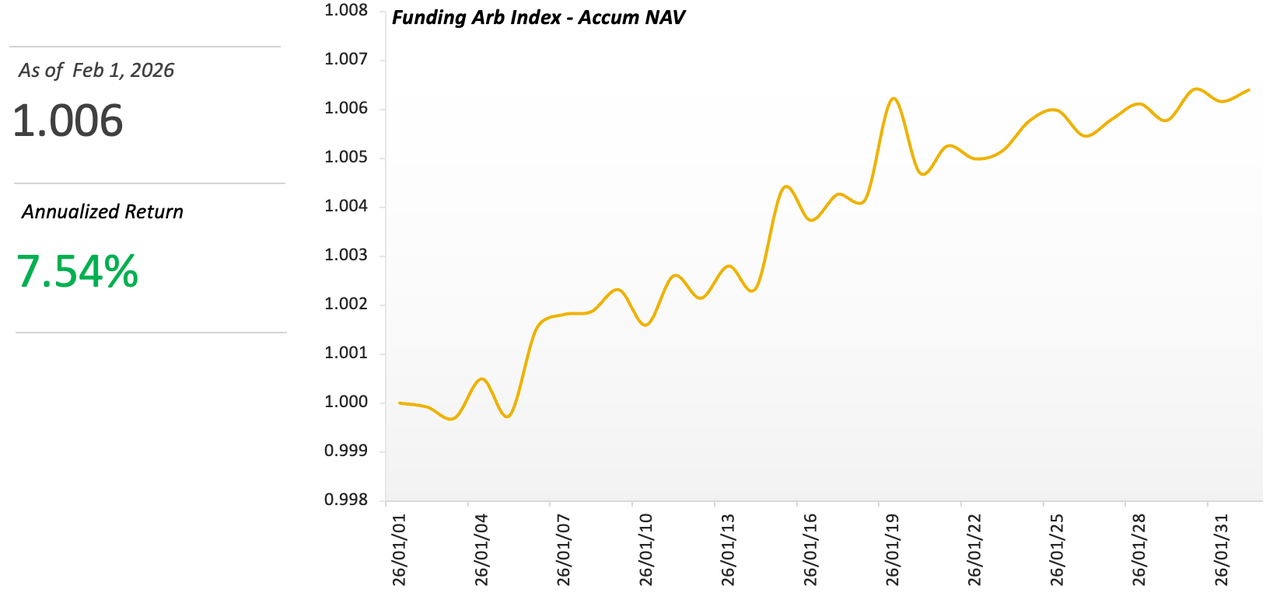

We have retrieved the assets of multiple crypto trading teams to the same starting point (January 1st at UTC 0) utilizing a historical retrieving mechanism, calculating the accumulated NAV for each team using the TWR (Time-Weighted Return) measure, and then taking the arithmetic mean to derive an index benchmark that represents the market’s Funding Arbitrage.

Note: We use the arithmetic mean instead of the weighted average because the current sample size is relatively small, and the weights in a weighted average cannot accurately reflect the actual weights of the trading team. Therefore, the impact of principal has been normalized.

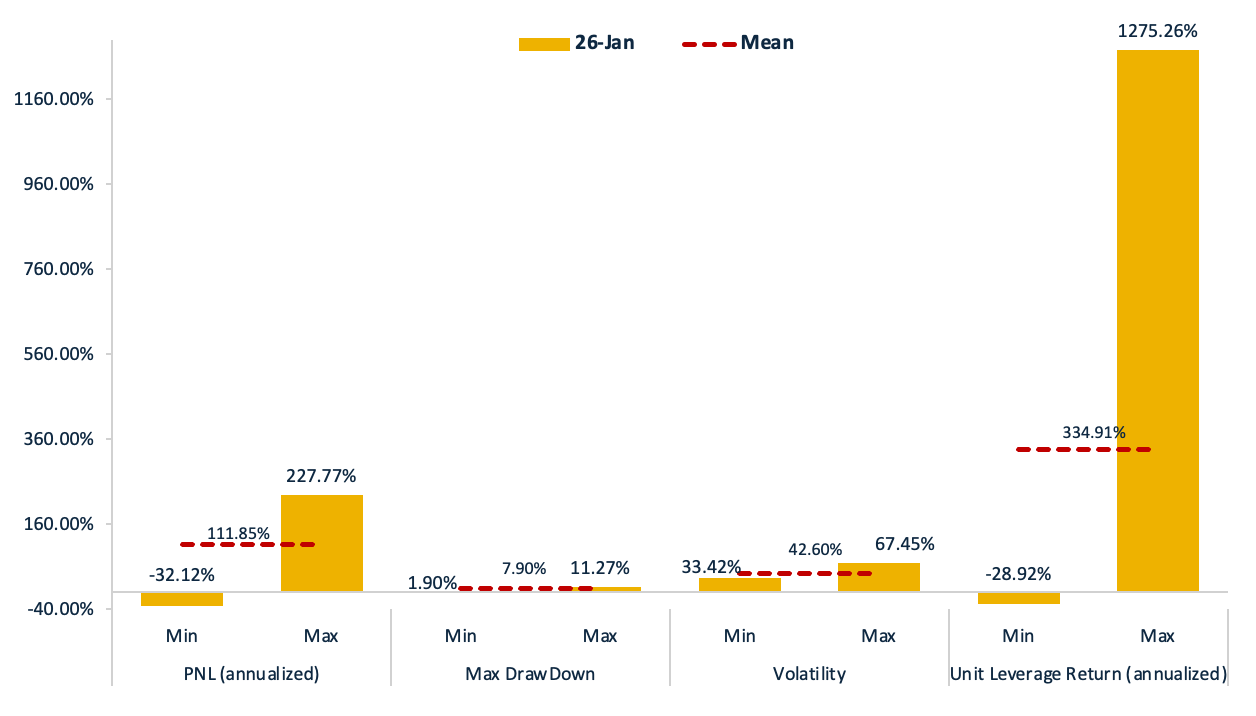

Indicators

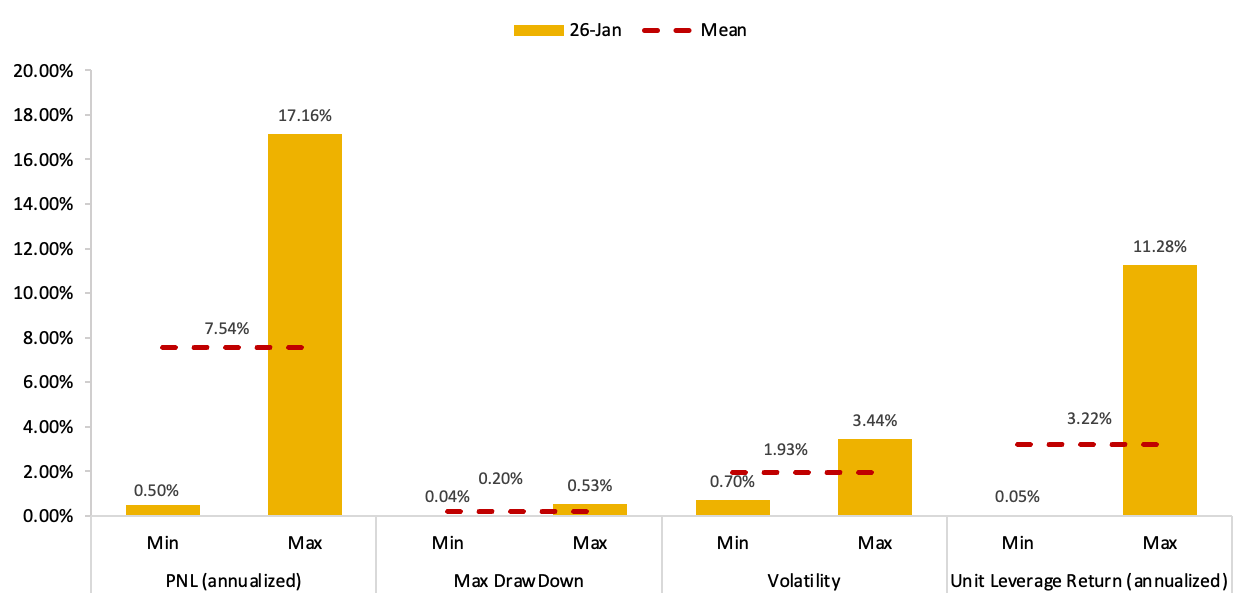

Given the relative stability of Funding Arbitrage, the Sharpe Ratio is not included in the scope of this study. Instead, we have selected 1-2 metrics from four perspectives—returns, risk, strategy characteristics and investment preferences—for market reference.

Profit and Loss (PNL) and Risk

Note: See Index Formula for full methodology and calculations.

Strategy Features

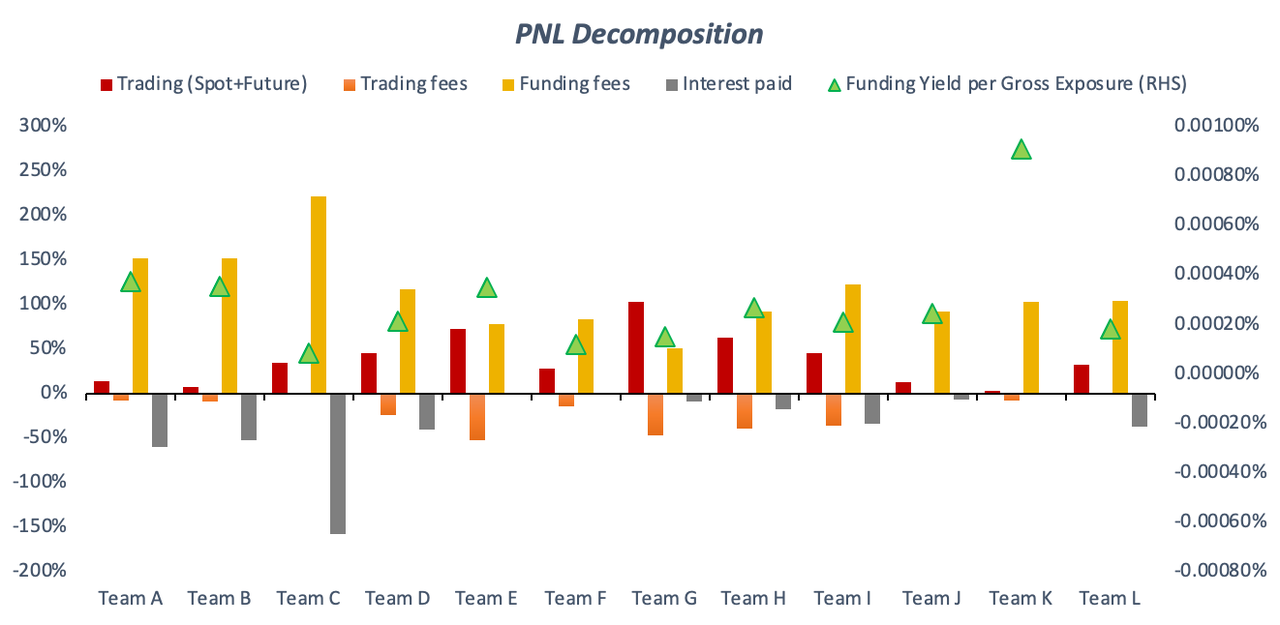

The perpetual contract funding rate management capability serves as a critical performance indicator for Funding Arbitrage strategies. In this report, we analyze January 2026 execution records across all participating teams, decomposing strategy returns into discrete components including funding income, trading fees, interest paid, and trading P&L. A higher proportion of funding income relative to total returns reflects greater proficiency in funding rate management.

To further enhance the evaluation framework, we introduce a new standardized metric: Funding Yield per Gross Exposure (FYpGE). This KPI measures funding income generated per unit of gross exposure. Higher FYpGE values demonstrate specialized expertise in capturing funding fees.

Note:

- The PNL Decomposition is calculated using various records to generate detailed PNL data, breaking down portfolio performance into individual components.

-

See

Index Formula

for full methodology and calculations.

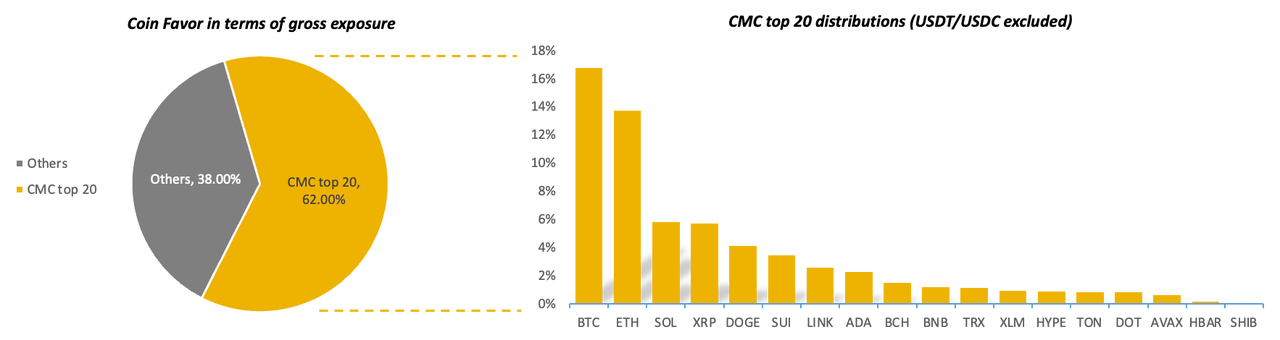

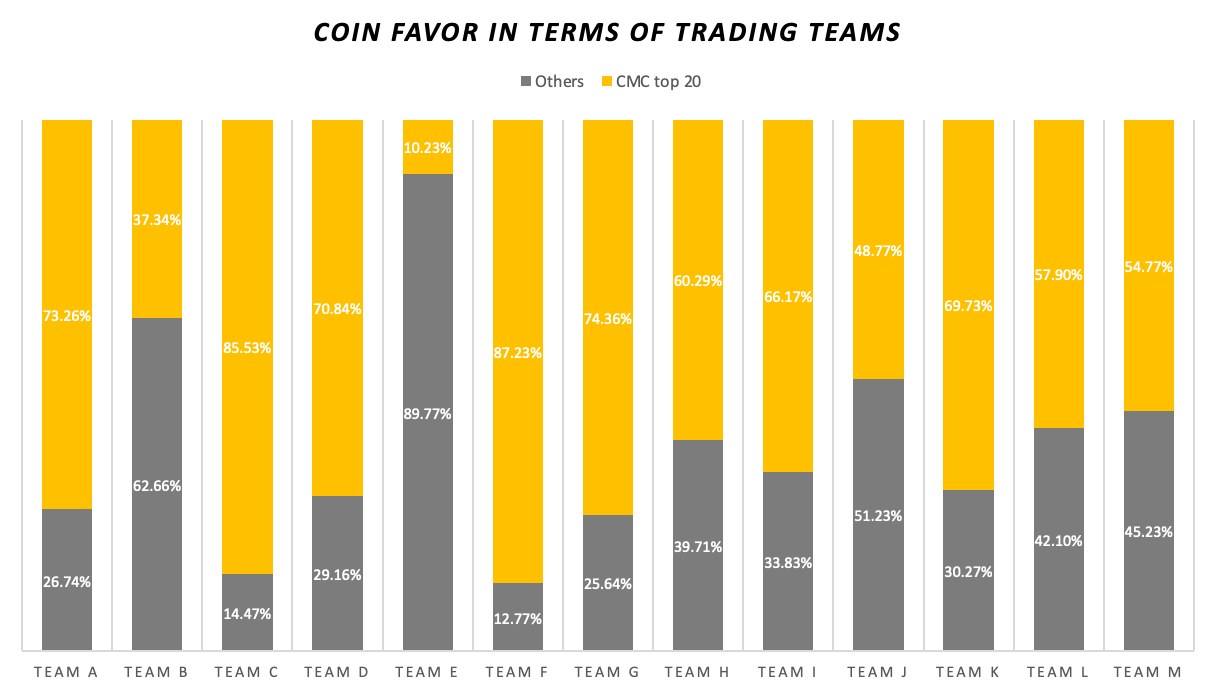

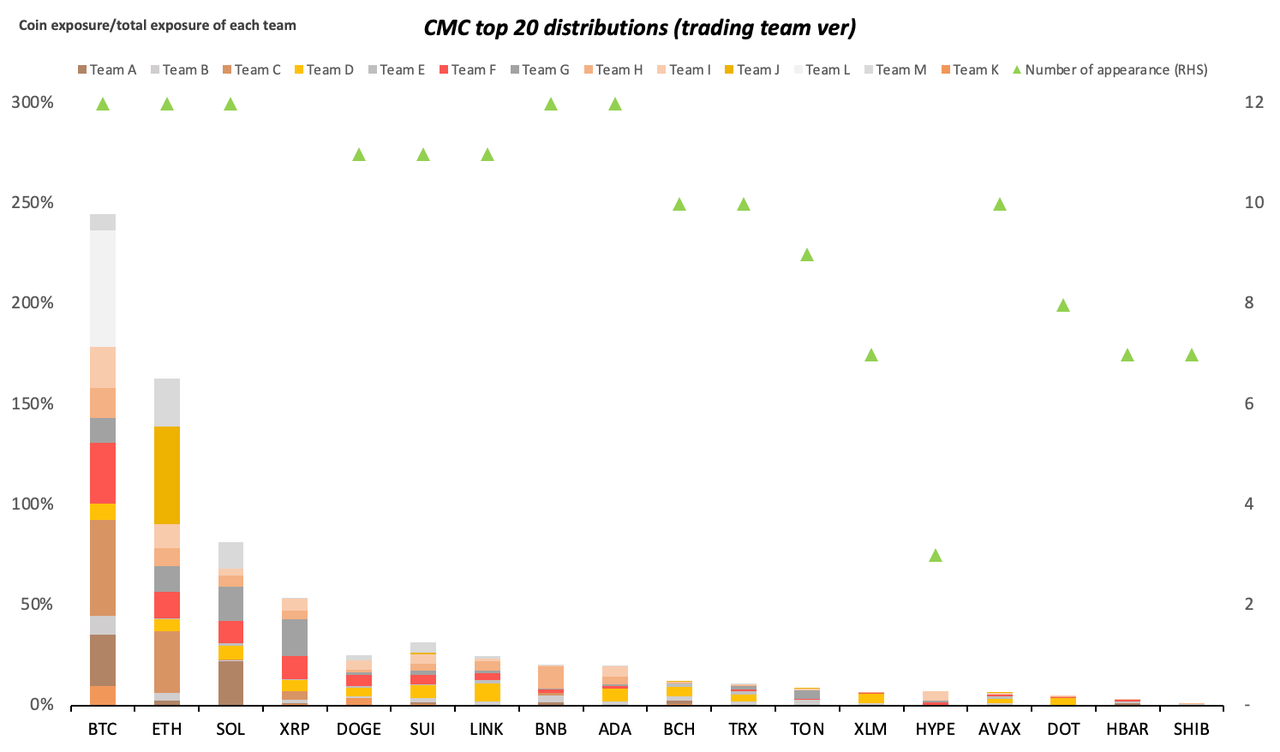

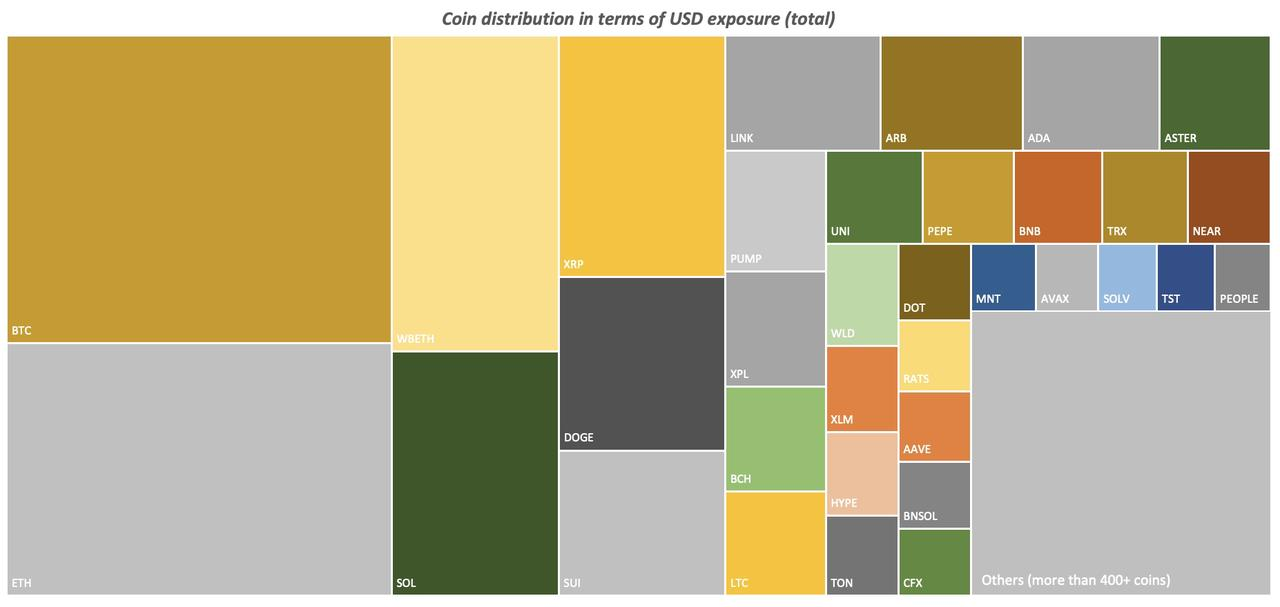

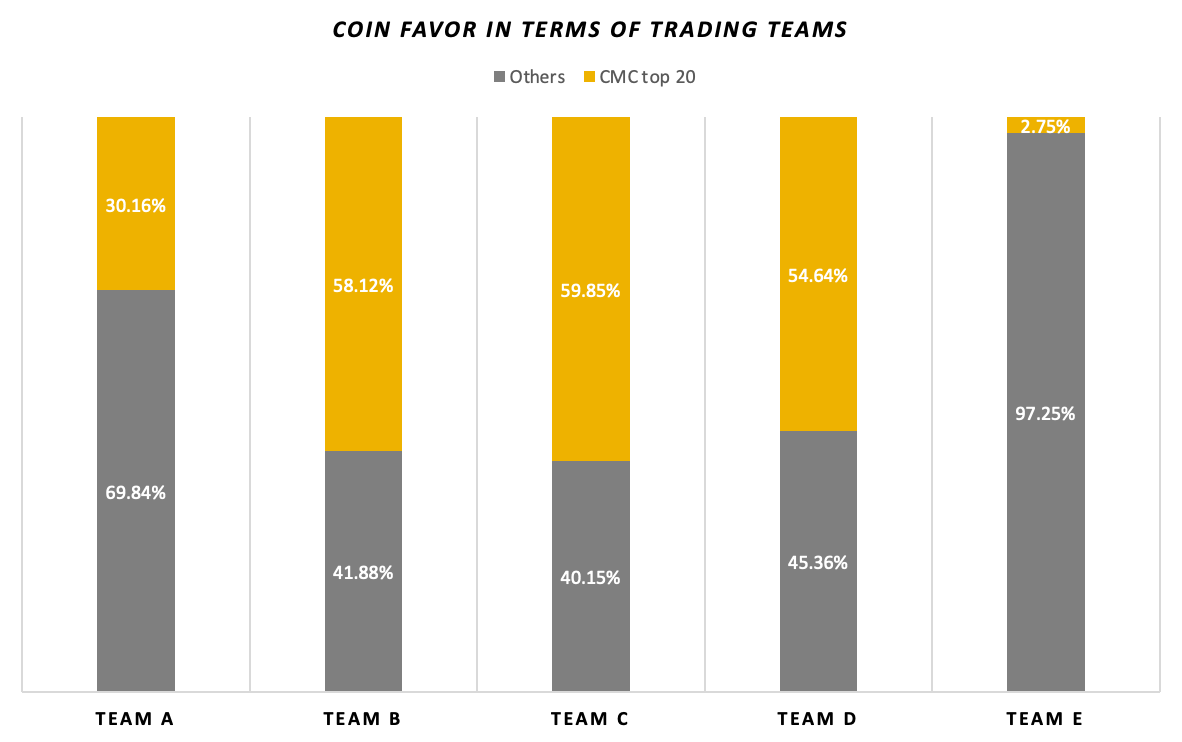

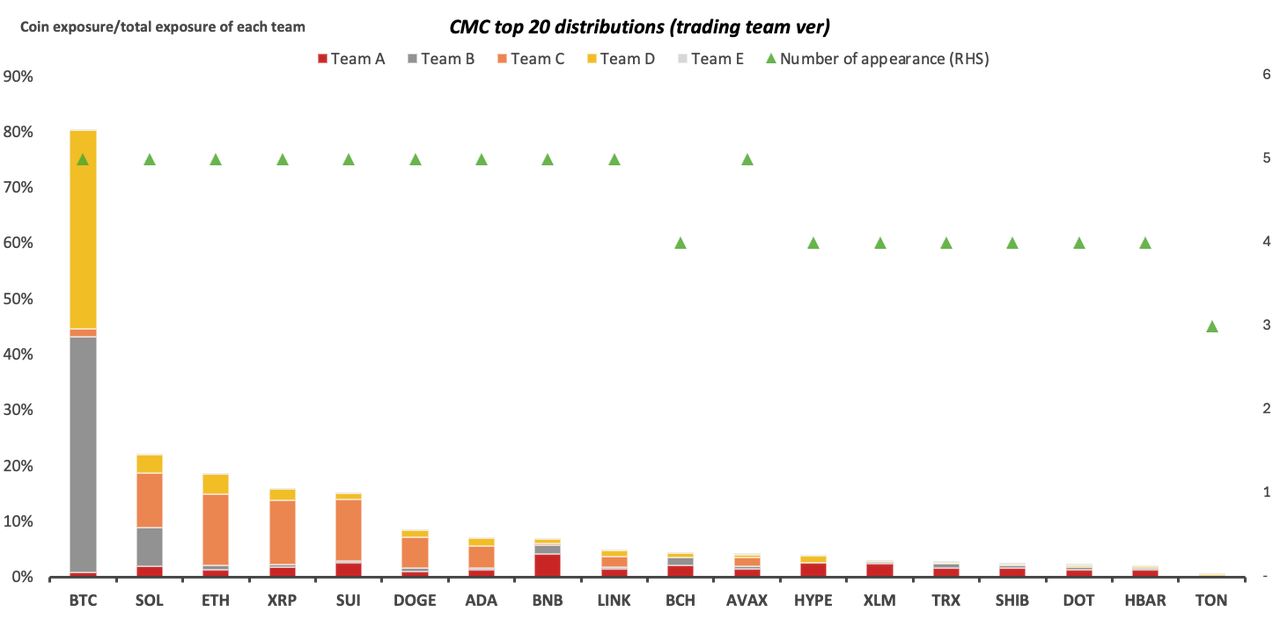

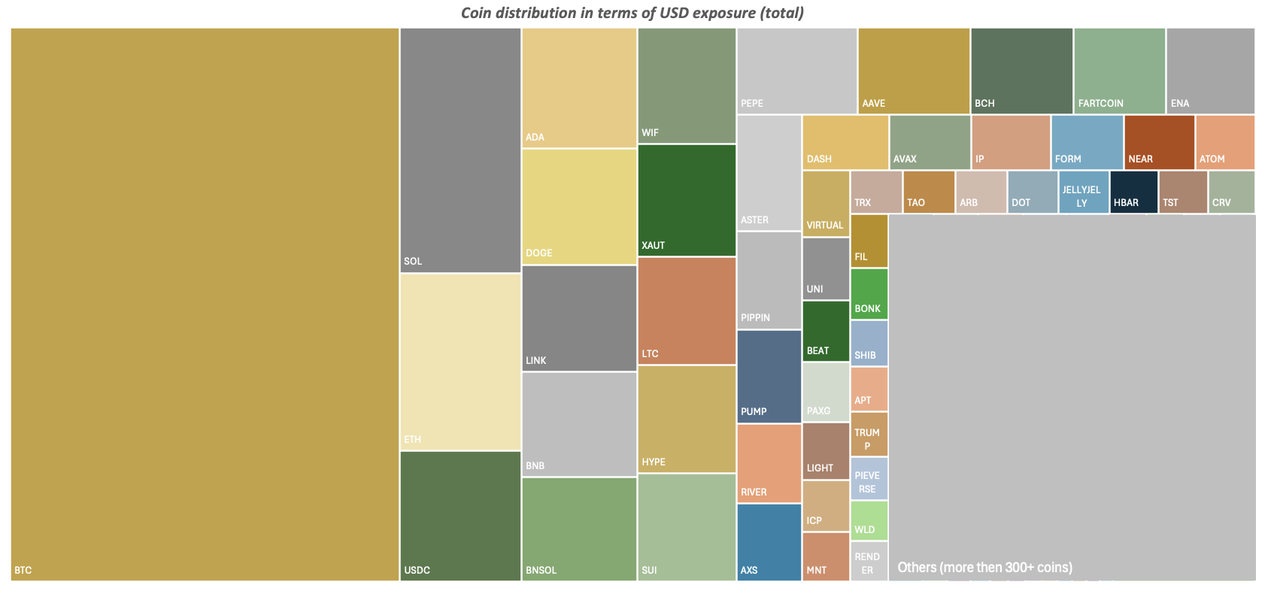

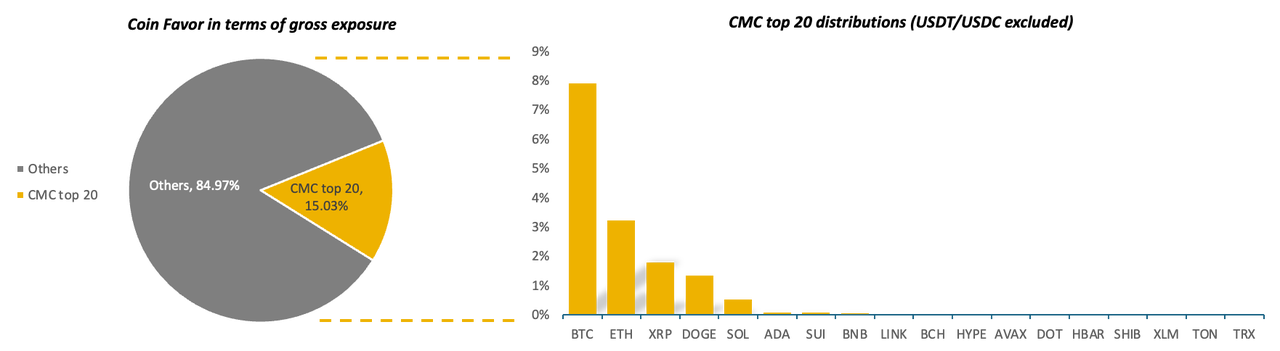

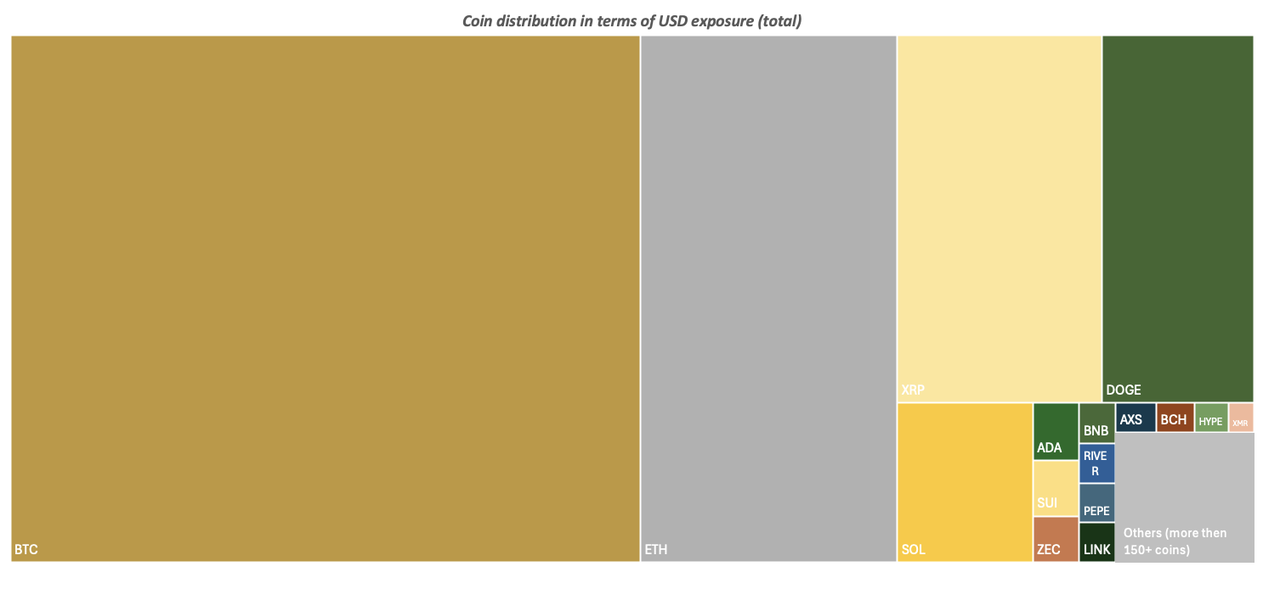

Coin Distributions

We have combined daily snapshot data from trading teams to summarize the asset positions from January 1st, 2026, at 00:00 UTC to February 1st, 2026, and aggregated the USD exposure for each underlying currency based on the underlying assets.

Note:

- USD exposure = Delta * Underlying Price

- See Index Formula for full methodology and calculations.

To assess the dispersion across coins, we defined the aggregation degree β (ranging from 0 to 1). When β is closer to 1, it indicates that the investment is more concentrated in a few coins, while when β is closer to 0, it indicates that the investment is more diversified.

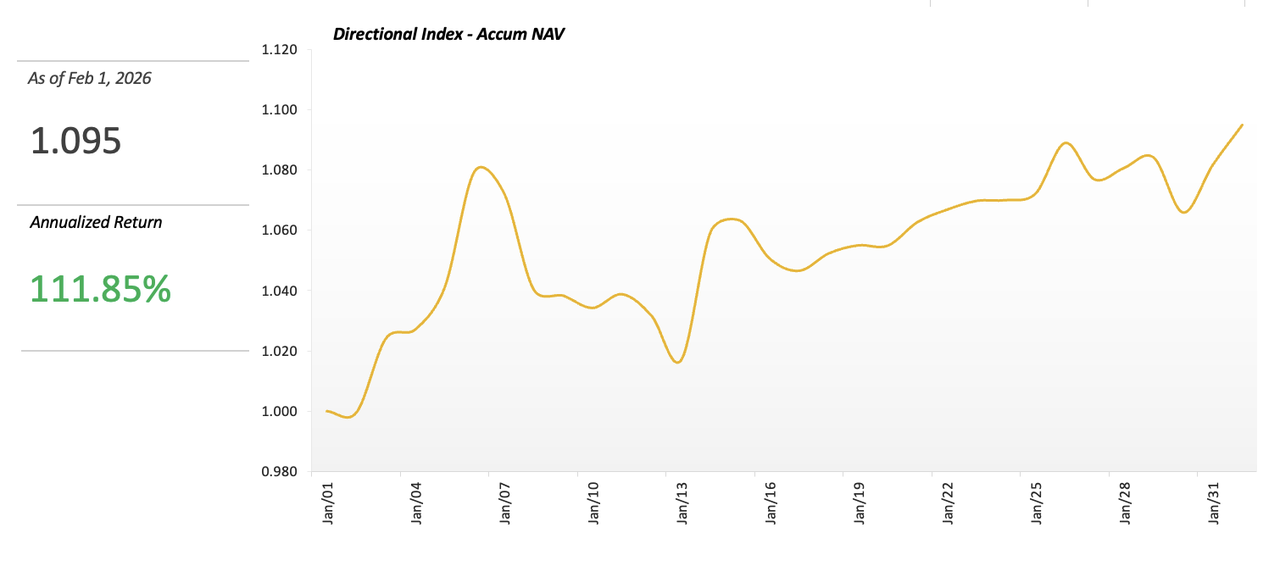

Index

Calculation method

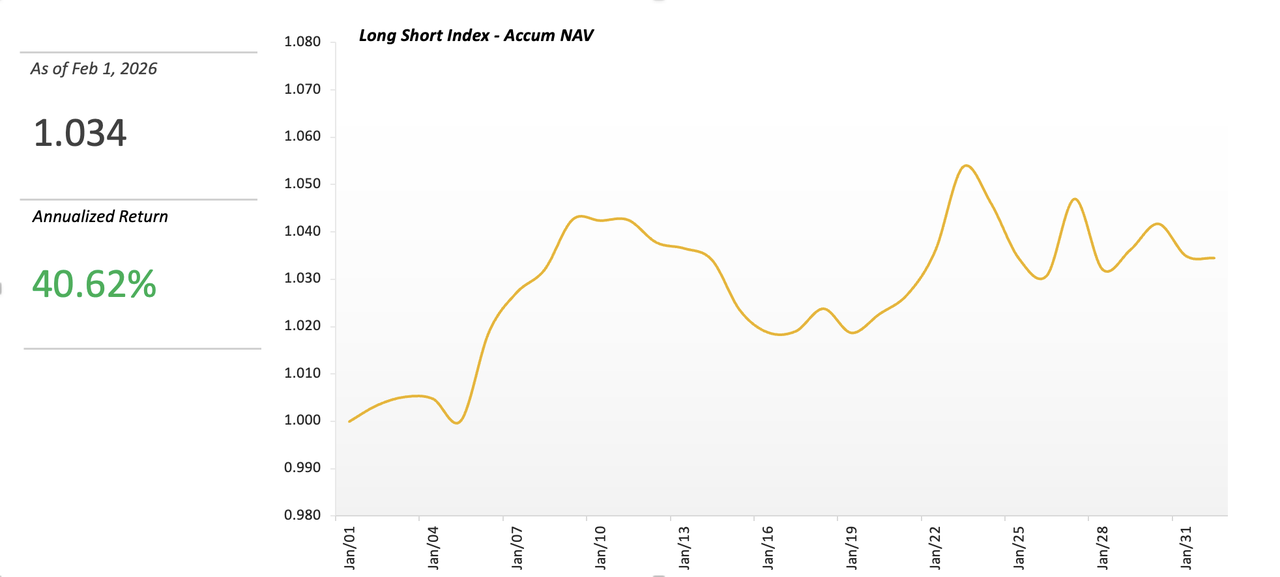

We have retrieved the assets of multiple crypto trading teams to the same starting point (January 1st at UTC 0) utilizing a historical retrieving mechanism, calculating the accumulated NAV for each team using the TWR (Time-Weighted Return) measure, and then taking the arithmetic mean to derive an index benchmark that represents the market’s Long Short strategy.

Note: We use the arithmetic mean instead of the weighted average because the current sample size is relatively small, as weighted averages cannot accurately reflect actual team weights. Therefore, the impact of principal has been normalized.

Indicators

Given the diversity of long-short strategies, this report provides a comprehensive analysis across four key dimensions—returns, risk exposure, strategy characteristics, and coin distributions—to offer market insights.

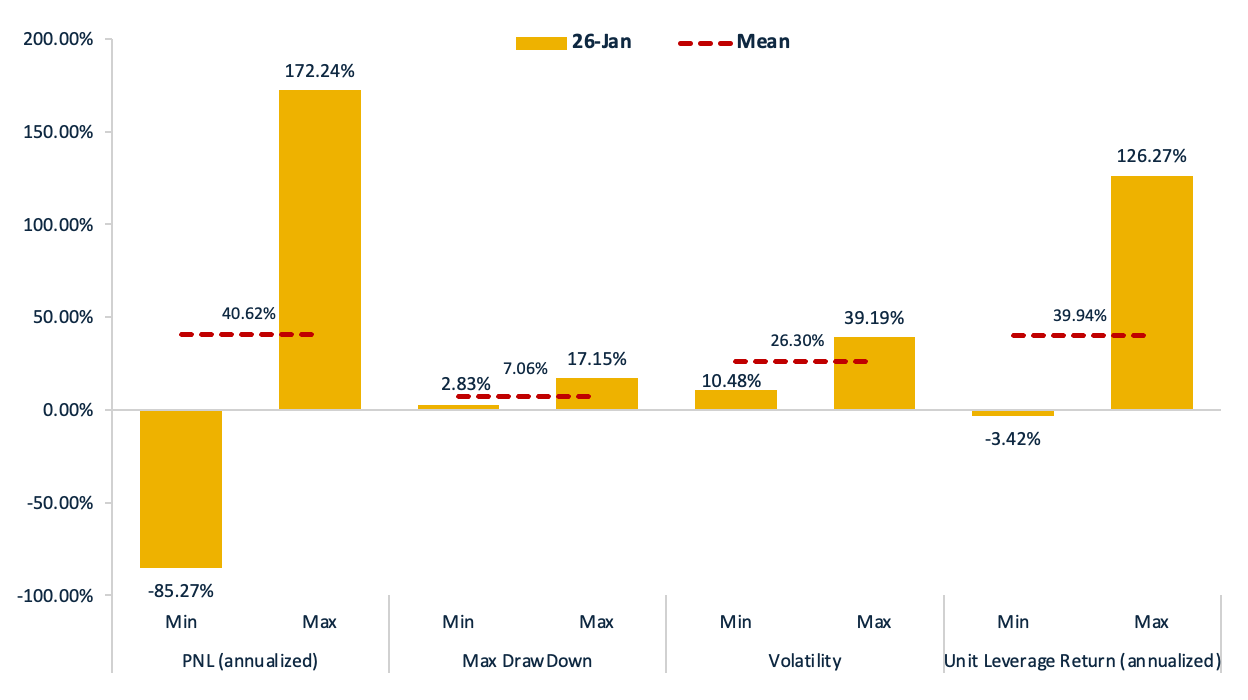

Profit and Loss (PNL) and Risk

Note: See Index Formula for full methodology and calculations.

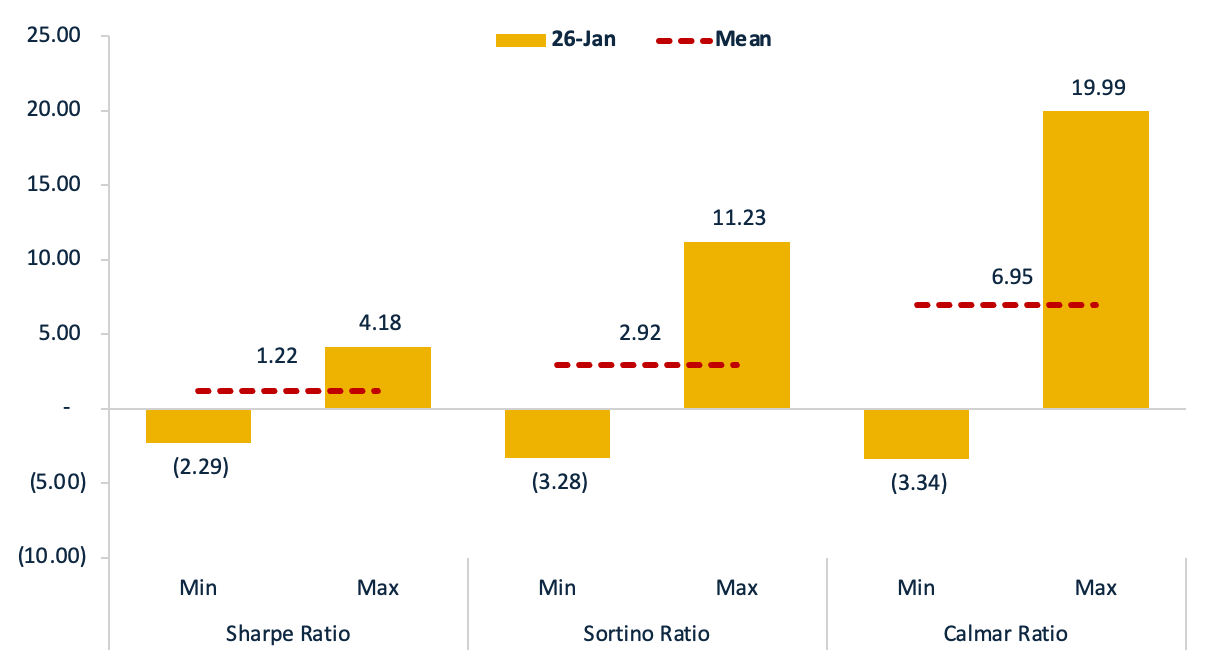

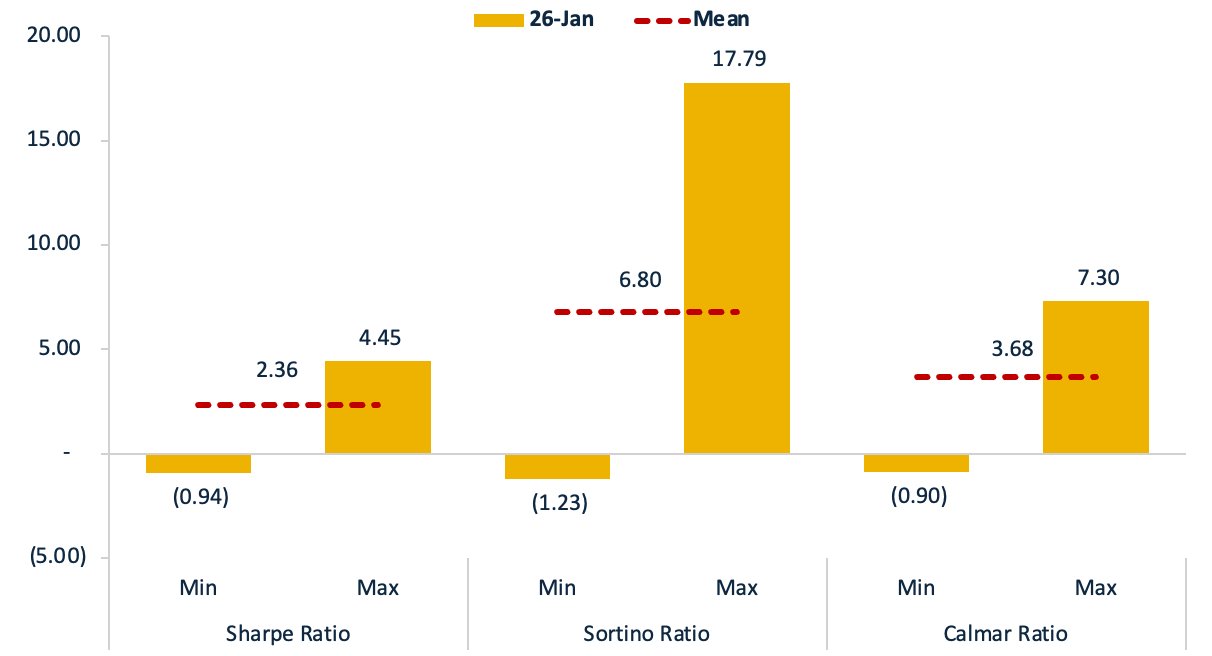

We further assessed risk-adjusted performance through Sharpe Ratio (measuring return per unit of total risk), Sortino Ratio (focusing specifically on downside risk), and Calmar Ratio (evaluating returns relative to maximum drawdown), providing a comprehensive framework to gauge strategy effectiveness across varying market environments.

Note: See Index Formula for full methodology and calculations.

Strategy Features

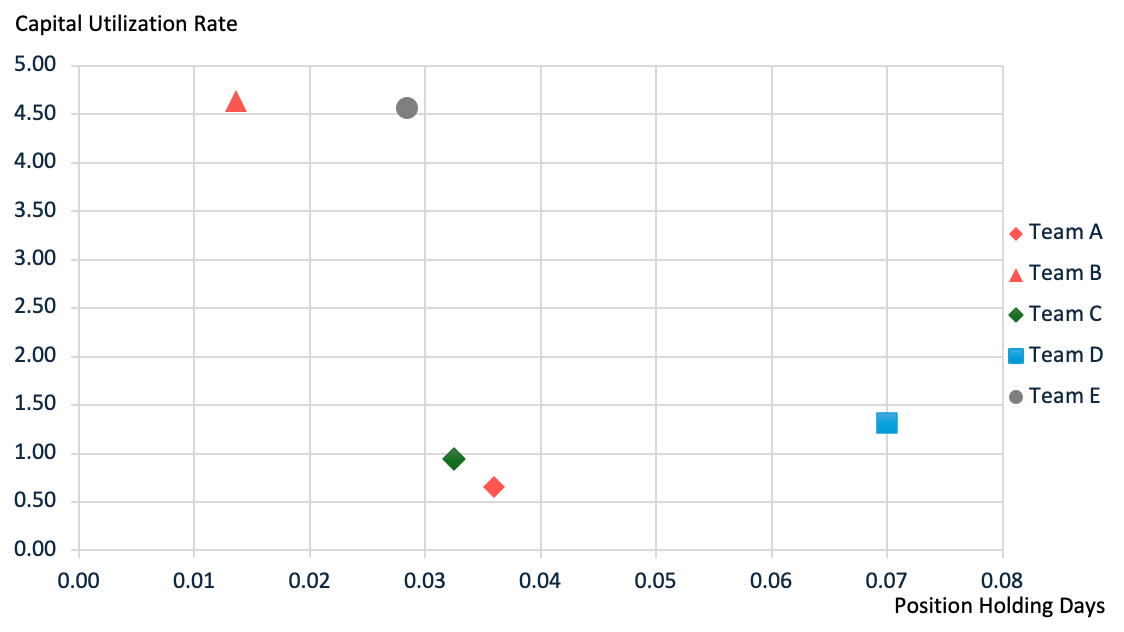

This section introduces two key liquidity metrics for Long Short strategy evaluation: Position Holding Days and Capital Utilization Rate(Turnover Rate).

👍 Position Holding Days serves as a key metric for evaluating capital efficiency.

Key characteristics:

- Inverse relationship with liquidity: Lower turnover days indicate higher strategy liquidity

👍 Capital Utilization Rate measures capital efficiency like turnover rate, but also incorporates margin.

Key characteristics:

- Liquidity indicator: Higher ratios reflect more efficient capital deployment

The multi-team dataset analysis reveals that long-short strategies exhibit superior liquidity performance, as demonstrated by consistently shorter position turnover cycles and higher capital utilization rates. The results across both metrics provide robust evidence for the liquidity benefits inherent to long-short strategy structures.

Note: See Index Formula for full methodology and calculations.

Coin Distributions

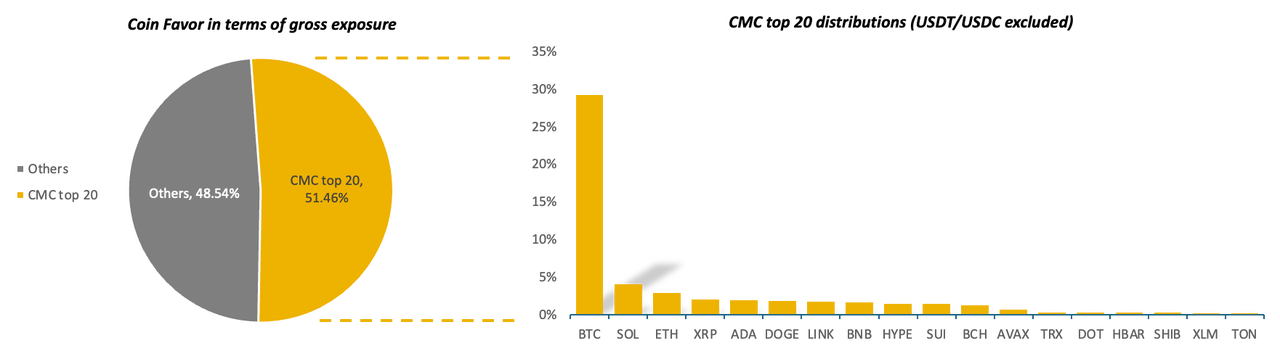

We have combined daily snapshot data from trading teams to summarize the asset positions from January 1st, 2026, at 00:00 UTC to February 1st, 2025, at 00:00 UTC, and aggregated the USD exposure for each underlying currency based on the underlying assets.

Note:

- USD exposure = Delta * Underlying Price

- See Index Formula for full methodology and calculations.

To assess the dispersion across coins, we defined the aggregation degree β (ranging from 0 to 1). When β is closer to 1, it indicates that the investment is more concentrated in a few coins, while when β is closer to 0, it indicates that the investment is more diversified.

Note: We use the arithmetic mean instead of the weighted average because the current sample size is relatively small, and the weights in a weighted average cannot accurately reflect the actual weights of the trading team. Therefore, the impact of principal has been normalized.

Indicators

Profit and Loss (PNL) and Risk

Note: See Index Formula for full methodology and calculations.

For a strategy defined by its volatility exposure, rigorous risk-adjusted assessment is critical. We employ the Sharpe Ratio to capture return per unit of total risk, the Sortino Ratio to isolate downside performance, and the Calmar Ratio to contextualize returns against peak-to-trough drawdowns. This multi-metric framework enables a nuanced evaluation of directional strategies' efficiency in harvesting macro beta while managing tail risks.

Note: See Index Formula for full methodology and calculations.

Strategy Features

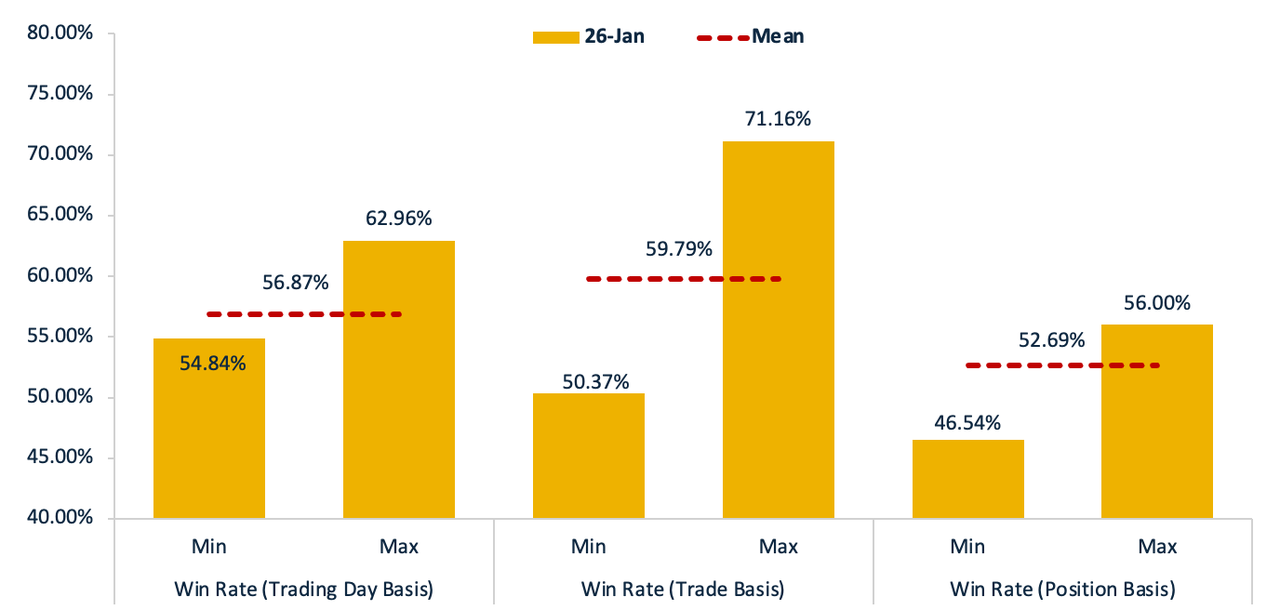

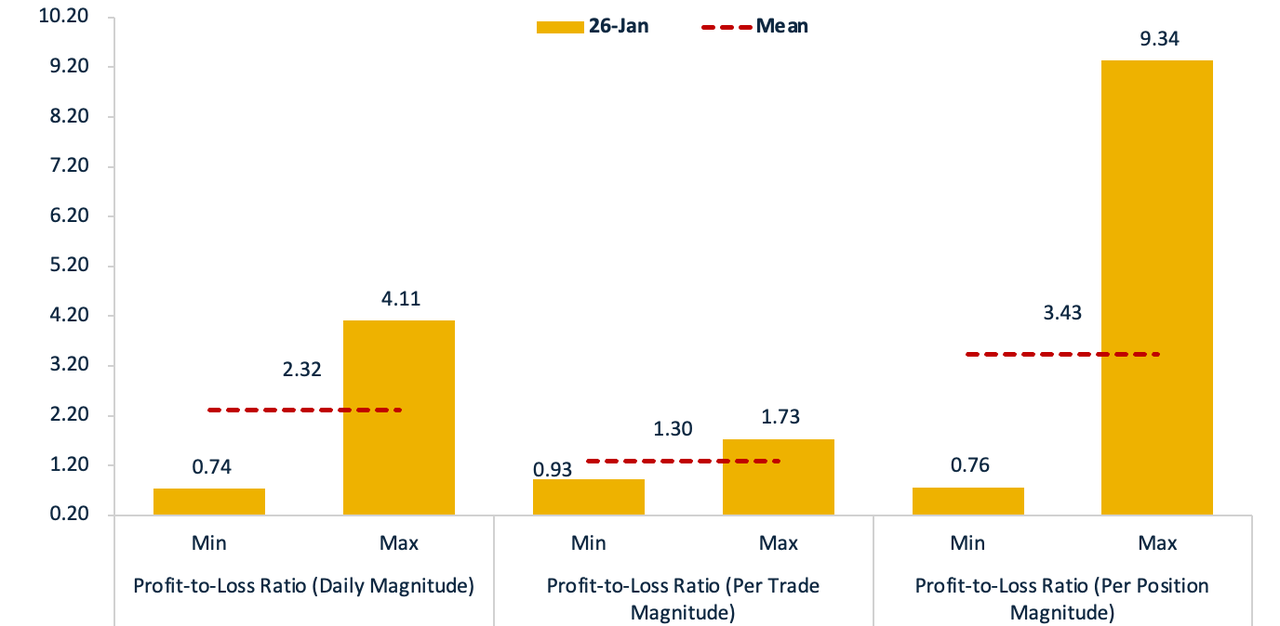

In addition to conventional return and risk metrics, the win rate and profit-to-loss ratio form the core profitability equation in directional—directly shaping the long-term risk-return profile.

Given the crypto market's high volatility and constant oscillation between trending and range-bound regimes, rigorous assessment of both metrics is essential. We conduct a multi-dimensional quantitative analysis—examining daily return distributions, position sizing dynamics, and individual trade entry/exit records—to derive the strategy's realized win rate and profit-to-loss ratio.

This framework systematically measures trend-capture efficiency, risk management discipline, and performance stability across market regimes, offering critical inputs for strategy optimization and capital allocation.

Note: See Index Formula for full methodology and calculations.

Coin Distributions

We have combined daily snapshot data from trading teams to summarize the asset positions from January 1st, 2026, at 00:00 UTC to February 1st, 2025, at 00:00 UTC, and aggregated the USD exposure for each underlying currency based on the underlying assets.

Note:

- USD exposure = Delta * Underlying Price

- See Index Formula for full methodology and calculations.

To assess the dispersion across coins, we defined the aggregation degree β (ranging from 0 to 1). When β is closer to 1, it indicates that the investment is more concentrated in a few coins, while when β is closer to 0, it indicates that the investment is more diversified.

The total AUM of the teams we collaborate with has exceeded $10 billion. In the future, we aim to increase the number of teams we monitor, along with the total AUM, which will also lead to a noticeable improvement in diversity.

Authored by Quinn Hu and Gloria Yao from 1Token, with data kindly provided by nine trading teams.

Reference

Thanks to the following leading crypto trading teams for collaborating with 1Token on our first crypto strategy-related performance analysis:

-

Bamboo

- Directional

- Bamboo Capital is founded on a "lean and elite" principle, consisting of 8 core members. Key members have previously held positions at Citadel and other leading domestic quantitative hedge funds.

- The team operates a core predictive model powered by deep learning, supported by over 200 alpha factors derived from order book and tick-by-trade data. Rigorous portfolio optimization controls asset weights and net exposure, while an ultra-low latency trading system ensures execution quality near VWAP benchmarks.

- Risk management is embedded through a comprehensive framework. Pre-trade risk metrics are converted into optimization constraints covering position weights, net exposure, and market impact. Real-time monitoring tracks latency, slippage, and uniMMR across all accounts 24/7, with automated escalation based on alert levels.

-

Binquant

- Funding Arb

- Founded in 2018, Binquant focuses on quantitative development and asset management in the digital asset market and is now one of the largest digital asset managers. The main strategies include market-neutral arbitrage, CTA, high frequency, and DeFi. Main clients include hedge funds, VC funds, large financial institutions, family offices, and exchanges for asset accretion.

-

DSG

- Directional

- DSG Tech is a quantitative investment firm specializing in systematic trading across digital assets. The firm applies a multi-strategy approach spanning trend-following CTA, cross-sectional long-short relative value, high-frequency market maker and arbitrage, with a focus on liquid markets and efficient execution. Its investment process is grounded in rigorous empirical research, disciplined risk controls, and continuous refinement of models and infrastructure, with the objective of producing uncorrelated and repeatable returns over time.

-

Grandline

- Funding Arb and Long Short

- GrandLine Technologies is a systematic multi-strategy trading firm established in 2018. Grandline specializes in deploying mid-frequency market-neutral strategies across major digital assets on both centralized and decentralized exchanges. With decades of expertise in quantitative portfolio management , the team is recognized for its exceptional research and risk management process, earning accolades from esteemed institutions like Hedgeweek and HFM.

-

Ladder Research

- Funding Arb

- Ladder Research is a quantitative trading firm founded in 2022, focused on delta-neutral arbitrage strategies across markets. The core team has been active in the industry since 2018, with deep experience in exchange microstructure, execution, and risk management.

- Ladder Research operates under a risk-first philosophy, aiming to deliver stable and scalable returns through disciplined execution and long-term iteration.

-

Lattice Research

- Long Short

- Lattice Research is a specialized asset manager focused on systematic trading strategies. Founded in 2022, we bring over 10 years’ experience from traditional finance to the crypto markets.

- The team comprises talents from leading institutions such as JP Morgan, Millennium, and HRT. Backed by multi-billion dollar funds and family offices, we have established a solid foundation in advanced machine learning technologies, low-latency infrastructure, and a comprehensive database coverage.

- At the core of our culture is a research-driven approach. We prioritize risk management over pure return generation, with the goal of delivering consistent, risk-adjusted performance for our investors.

-

Lepton

- Funding Arb

- Founded in 2021 by seasoned quant traders with 10+ years of arbitrage expertise in traditional finance, we specializes in systematic crypto arbitrage strategies. Our proprietary low latency execution system enables algorithmic capture of funding rate arbitrage, basis arbitrage, and market making opportunities within CEX venues. Through adaptive risk frameworks and dynamic exposure management, we maintain rigorous operational discipline to proactively mitigate tail risks while exploiting transient market inefficiencies.

-

Luxtech

- Funding Arb

- Luxtech Capital Group Ltd was established in 2018 by a group of fund managers from both domestic and international backgrounds. Focused on the meticulous study of quantitative strategies, we utilize mathematical models and computer technology to discover robust quantitative strategies that transcend market fluctuations. Our expertise lies in asset management for digital assets. Shareholders and team members are derived from the professional traditional asset management industry, with a cumulative managed fund scale exceeding 10 billion RMB, and their collective experience is traceable. Research personnel hold Master's and Ph.D. degrees from renowned universities such as the University of Illinois at Urbana-Champaign, Tsinghua University, and Shanghai Jiao Tong University. They have previously worked in core departments at Akuna Capital and Citadel, demonstrating solid foundational knowledge and extensive experience in the quantitative industry.

-

JZL

- Funding Arb

- JZL Capital, specializing in Spot-Perpetual Arbitrage, is a top-tier quantitative team in Asia providing stable return performance and achieving over $200 million in AUM. The core team comprises members passionate about academic research and actively expanding its global client base by providing unparalleled quantitative trading solutions.

-

Pythagoras

- Funding Arb and Long Short

- Established in 2014, Pythagoras manages a suite of crypto funds based on quantitative modeling. As one of the longest-running crypto hedge funds, it is known for delivering outstanding returns in both bearish and bullish market cycles. Using systematic, non-discretionary, and automated trading strategies, Pythagoras specializes in market-neutral and dollar-neutral strategies to consistently outperform the crypto market.

-

Tackzone

- Funding Arb

- Tackzone Research is a quantitative research and strategy management fund focused on the digital asset market. We are committed to delivering stable and sustainable return solutions for investors through systematic strategies, rigorous risk controls, and efficient execution.

- With long-term expertise in crypto derivatives and arbitrage, the team conducts quantitative research across funding rates, spread structures, liquidity conditions, and market microstructure, and has built an automated trading system spanning multiple exchanges and diverse strategy types.

- We have established a full end-to-end closed loop covering strategy R&D, backtesting and evaluation, live trading operations, and risk management, ensuring disciplined implementation and continuous improvement across the entire investment lifecycle.

-

KFQuant

- Funding Arb

- Founded in 2017, KFQuant is a top low-latency trading systems provider from traditional finance, powering a significant share of multi-billion-dollar hedge funds and proprietary trading desks. Specializing in ultra-fast systems and cross-sectional multi-factor strategies—hallmarks of traditional finance. We integrate tick-by-tick data, alternative alpha signals, streaming-learning models, and automated portfolio optimization into a seamless research-to-execution pipeline. Our market-neutral derivatives long-short strategies deliver high capacity and Sharpe ratios, combining institutional-grade infrastructure with cutting-edge quantitative frameworks to sustain uncorrelated returns across cycles.

-

ZenX

- Long Short

- ZenX was founded in 2019 and is headquartered in Hong Kong. ZenX is an innovative and established crypto trading firm with a focus on cutting-edge technology, data-driven solutions, and algorithmic modeling. We aim to build long-term relationships with clients by offering tailor-made services with professional trading expertise.

Collaboration teams for this study primarily come from Asia. In the future, we hope to expand the diversity of our sample to include teams across various regions around the world. If you'd like to be part of our benchmark study, please feel free to contact our partnership manager at joey.shi@1tokentech.com.

About 1Token

1Token(https://1token.tech/) is a SOC2 Compliant software for institutional Crypto Portfolio, Risk, Operations, Accounting and Lending Management, named Hedgeweek's 2024 "Portfolio Management Solution of the Year", serving 100+ top-tier institutional clients in the crypto industry, including Family Offices, SMA Allocators, Multi-Strategies Trading Funds, DMA Prime Brokers, Asset Managers, Lending Institutions, Fund Admins & Auditors across the US, EU, and APAC, collectively managing over $20 billion in assets.

For general inquiries like authorization requests of the report, product demo, or general collaboration opportunities, please email service@1token.trade.

Disclaimer

The information contained in this report is provided by 1Token for general informational purposes only and does not constitute professional advice. While every effort has been made to ensure the accuracy of the information, no warranty or representation, express or implied, is made regarding its completeness or reliability. The contents of this report reflect the views and opinions of the author(s) as of the date of publication, and may be subject to change without notice.

The reader should independently verify any information or conclusions presented herein before making decisions based on the report. 1Token and any affiliated parties are not responsible for any actions taken or not taken as a result of reading this report.

This report may contain forward-looking statements, estimates, and projections based on current expectations. These statements are subject to risks and uncertainties that could cause actual results to differ materially from those anticipated. 1Token assumes no obligation to update or revise any forward-looking statements.

Comments ()